Running a business is thrilling. You get to bring your vision to life, serve your community, and be your own boss. But the financial administration? For many entrepreneurs, that is often the least glamorous part of the job. However, mastering small business bookkeeping is the absolute backbone of a healthy, growing enterprise. Whether you are selling handmade crafts out of a home studio or running a rapidly expanding tech startup, understanding the numbers is what keeps the lights on.

Many founders treat financial record-keeping as an afterthought, scrambling when tax season approaches. But with the right strategies, bookkeeping for small business transitions from a chaotic, anxiety-inducing chore into a powerful tool for strategic growth. In this comprehensive guide, we will break down the essential practices to help you take total control of your finances, make informed decisions, and set your company up for long-term success.

Summary

This guide covers the bookkeeping fundamentals—choosing cash vs. accrual methods, single vs. double-entry systems, and building a clear chart of accounts—along with selecting modern, cloud-based software. It emphasizes consistent daily and weekly habits for expense capture and cash-flow management, plus monthly and quarterly tasks like reconciliations, payroll, and estimated taxes. You’ll learn to interpret key financial statements to drive decisions and know when to delegate as you scale. A practical checklist ties it all together to build discipline, ensure compliance, and support sustainable growth.

Laying the Foundation for Your Finances

Before you start logging receipts and sending out invoices, you need to establish the basic structural rules of your financial ecosystem. Making the right choices early on saves you from massive headaches and costly accountant bills later.

Choosing Your Method: Cash Basis vs Accrual

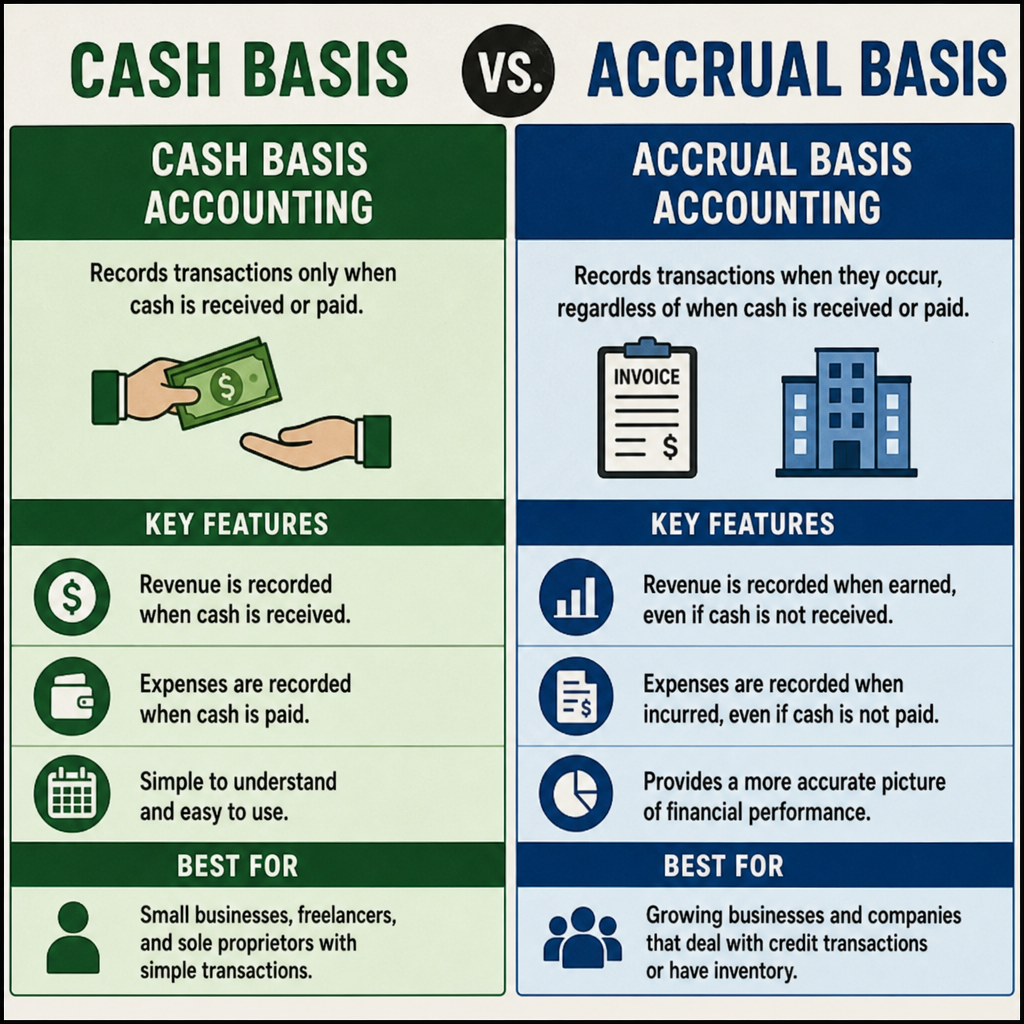

One of the very first decisions you will face is evaluating cash basis vs accrual accounting methods. Your choice here dictates how and when you record your financial transactions.

- Cash Basis: This method is straightforward and highly popular for small company bookkeeping. You simply record revenue when the money physically hits your bank account, and you record expenses when the cash actually leaves your account. It is intuitive and makes tracking your immediate cash flow easy.

- Accrual Accounting: This method records income and expenses when they are billed or incurred, regardless of when the cash actually moves. For example, if you send an invoice in November but get paid in January, the income is recorded in November. While slightly more complex, accrual accounting provides a far more accurate long-term picture of your overall financial health.

Single-Entry vs Double-Entry Bookkeeping

Next, you need to understand the difference between single-entry vs double-entry bookkeeping.

Single-entry is like maintaining a traditional checkbook register. You record each transaction just once, either as incoming revenue or an outgoing expense. It works well for very small hobby businesses. Double-entry, however, is much more robust. In this system, every transaction gets entered twice—once as a debit in one account and once as a credit in another—keeping your books perfectly balanced. For any growing enterprise aiming for accuracy and scale, double-entry is the gold standard.

Structuring Your Accounts

To keep everything neatly organized, you must know how to set up a chart of accounts. Think of this as the master index or filing cabinet of all the financial accounts in your business. It is typically broken down into five main categories:

- Assets: What you own (cash, equipment, inventory).

- Liabilities: What you owe (loans, credit card balances).

- Equity: What is left over for the owner.

- Revenue: The money coming in from sales.

- Expenses: The costs of doing business (rent, utilities, payroll).

A well-structured chart of accounts allows you to categorize every single transaction accurately, making it much easier to generate meaningful financial reports later on.

Choosing the Right Digital Tools

Gone are the days of keeping physical ledgers, desktop calculators, and shoeboxes full of faded receipts. Today, leveraging modern technology is absolutely non-negotiable for efficient accounting for business.

The Shift to Specialized Software

Choosing the right business accounting software for small business can automate hours of tedious manual data entry, freeing you up to focus on what you do best. The market is incredibly diverse, offering something for every stage of growth.

If you are a solo operator, you might opt for lightweight accounting software for freelancers that focuses heavily on simple invoicing and basic expense tracking. Conversely, if you have employees and inventory, you will need more comprehensive software for small business accounting that offers advanced reporting and inventory management features. Look for platforms that integrate seamlessly with your business bank accounts, point-of-sale systems, and payment processors to minimize manual input.

The Power of the Cloud

When selecting your tools, do not overlook the massive cloud-based accounting system advantages. Unlike older software that lived on a single hard drive, cloud software allows you to access your financial data securely from any device with an internet connection. It automatically backs up your records, applies the latest security updates, and makes collaborating with a CPA or financial advisor incredibly easy. Furthermore, it ensures you are always looking at real-time financial data rather than outdated, static spreadsheets.

Daily and Weekly Small Business Bookkeeping Habits

Consistency is the secret ingredient to stress-free small business bookkeeping. Waiting months to catch up on your numbers is a recipe for disaster.

Tracking Expenses and Receipts

Do not wait until the week before tax day to sort through your spending. Organizing business receipts for tax season should be a continuous, year-round habit. By utilizing mobile apps that allow you to snap photos of receipts on the go, you can instantly digitize your records and link them to the corresponding bank transaction.

The automated expense tracking software benefits are massive in this area. Modern tools can use optical character recognition (OCR) to read your receipts and categorize your spending automatically. This ensures you are diligently tracking deductible business expenses—like travel, office supplies, and meals—without spending your weekends hunched over a desk. Missing out on legitimate deductions means leaving hard-earned money on the table, so meticulous tracking is vital.

Managing Cash Flow

Cash flow is the lifeblood of your company. Weekly check-ins are crucial for effectively managing accounts payable and receivable.

- Accounts Receivable: This is the money owed to you. Send prompt, clear invoices and establish a strict follow-up routine for overdue payments. The faster you invoice, the faster you get paid.

- Accounts Payable: This is the money you owe to vendors and suppliers. Scheduling your outward payments strategically prevents you from overdrawing your accounts while ensuring you maintain good relationships with your vendors by paying on time.

Monthly and Quarterly Must-Dos

While daily and weekly tasks keep the engine running, your monthly and quarterly routines ensure your business is actually heading in the right direction and staying legally compliant.

Bank Reconciliations

One of the most critical steps in your financial routine should be reconciling bank statements monthly. This process involves cross-checking your internal accounting records against your official bank and credit card statements to ensure they match perfectly, down to the penny.

Why is this so important? It helps catch bank errors, missed transactions, or even unauthorized fraudulent charges before they spiral out of control. Regular reconciliation is a fundamental pillar of general ledger maintenance best practices, keeping your core financial records pristine and trustworthy.

Payroll and Taxes

If you have a team, maintaining accurate payroll records is both a strict legal requirement and a moral obligation to your staff. Ensure that tax withholdings, employee benefits, and hours worked are meticulously documented and stored securely.

Furthermore, quarterly check-ins are essential for understanding quarterly estimated tax payments. Unlike traditional W-2 employees who have taxes withheld from every paycheck, most small business owners must calculate and pay their income and self-employment taxes four times a year. Failing to calculate these accurately—or missing the deadlines entirely—can result in hefty penalties and interest charges from the IRS.

Big Picture: Financial Management and Reporting

Good bookkeeping isn't just about satisfying the tax authorities; it is about gleaning actionable insights to grow your enterprise.

Generating and Analyzing Statements

Accurate daily data entry leads directly to accurate financial statement preparation for entrepreneurs. You should regularly review your core trio of financial reports:

- The Profit and Loss Statement (Income Statement): Shows your revenue minus your expenses over a specific period, revealing if you are actually turning a profit.

- The Balance Sheet: Provides a snapshot of your company's net worth at a specific moment, detailing your assets, liabilities, and equity.

- The Cash Flow Statement: Tracks how actual cash moves in and out of your business, highlighting your liquidity.

Regularly reviewing these statements helps you spot seasonal trends, identify bloated expenses that need cutting, and confidently forecast your future growth.

Knowing When to Delegate

As your business scales, your time becomes increasingly valuable. A task that once took an hour a week might suddenly require ten hours. Eventually, you will need to carefully weigh the pros and cons of outsourced vs in-house financial management.

Handling the books yourself is a great learning experience when you are just starting out. However, bringing in a professional fractional bookkeeper or an outsourced accounting firm can free up your schedule to focus on high-impact activities like sales, marketing, and product development. A professional will also ensure that your books are audit-proof, perfectly balanced, and fully compliant with ever-changing tax codes.

Your Ultimate Action Plan

To pull all of this information together, having a documented system is key. We highly recommend creating a structured bookkeeping checklist for new owners to help you stay disciplined.

Your Checklist Should Include:

- Daily: Review cash position, snap photos of business receipts, log daily sales.

- Weekly: Send out customer invoices, follow up on late payments, record and categorize vendor bills.

- Monthly: Reconcile bank and credit card accounts, review past-due accounts receivable, process payroll, and review your Profit and Loss statement.

- Quarterly: Review annual goals, file and pay quarterly estimated taxes, and check inventory levels.

Mastering your business finances does not happen overnight. It requires patience, the implementation of the right digital tools, and an unwavering commitment to consistency. By setting up a solid structural foundation, leveraging smart software, and maintaining regular financial habits, you transform bookkeeping from a stressful obligation into your greatest strategic advantage. Keep your records clean, monitor your cash flow closely, and watch your small business thrive.

Q&A

Question: How do I decide between cash-basis and accrual accounting?

Short answer: Choose cash-basis if you want simplicity and a clear view of immediate cash in and out—record income when you’re paid and expenses when you pay them. Choose accrual if you invoice customers or want a more accurate long-term picture—record income when earned and expenses when incurred, regardless of cash movement. Make this choice early to avoid costly headaches switching later.

Question: Is single-entry bookkeeping enough, and when should I use double-entry?

Short answer: Single-entry can work for very small, hobby-style operations because it’s like a checkbook—simple in/out tracking. For any growing business aiming for accuracy and scale, use double-entry. Recording every transaction as both a debit and a credit keeps your books balanced, improves reporting, and supports clean reconciliations.

Question: What features should I prioritize in accounting software, and why go cloud-based?

Short answer: Match the tool to your stage: freelancers need strong invoicing and basic expense tracking; businesses with employees or inventory need advanced reporting and inventory management. Prioritize integrations with your bank, POS, and payment processors to cut manual entry, plus mobile receipt capture and OCR for automatic expense categorization. Cloud-based systems add secure anytime access, automatic backups and updates, real-time data, and easy collaboration with your CPA.

Question: What bookkeeping routine should I follow to stay organized and compliant?

Short answer: Build a consistent cadence:

- Daily: Review cash position, snap photos of receipts, log sales.

- Weekly: Send invoices promptly, follow up on late payments, record and categorize vendor bills, and manage A/R and A/P to protect cash flow.

- Monthly: Reconcile bank and credit card accounts, review past-due receivables, process payroll, and review your Profit & Loss statement.

- Quarterly: Review annual goals, file and pay estimated taxes, and check inventory levels.

Monthly reconciliations are critical for catching errors or fraud early and keeping your general ledger trustworthy.

Question: When should I hand off bookkeeping to a professional?

Short answer: As your business scales and bookkeeping starts consuming high-value time—or your records feel chaotic—consider a fractional bookkeeper or outsourced firm. Delegating frees you to focus on sales, marketing, and product, while a pro keeps your books audit-proof, balanced, and compliant with changing tax rules, especially when paired with cloud tools for seamless collaboration.